Building a real estate portfolio on Long Island is defined by one core challenge: high entry costs demand a precise strategy, not a general one. Median home prices sit around $837,000 in Nassau County and $701,000 in Suffolk County as of early 2026. Those numbers are not a reason to walk away. They are a reason to choose your investment lane carefully, use the right financing tools, and understand the local tax and rental dynamics that determine whether a property generates wealth or drains it.

What are the best investment strategies to build a Long Island portfolio?

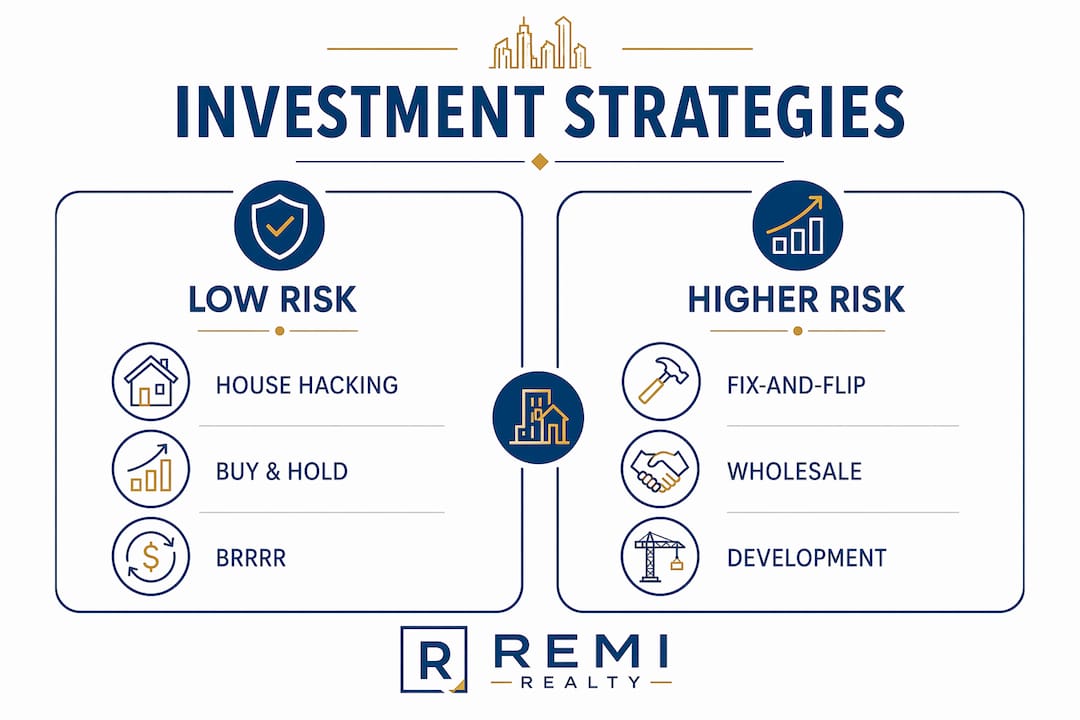

The right property investment strategy on Long Island depends entirely on your capital, time, and risk tolerance. No single strategy fits every investor, and that truth is especially sharp in a market this expensive and competitive. Here are the four strategies most relevant to Long Island conditions.

House hacking

House hacking is the most accessible entry point for new investors on Long Island. You purchase a multi-family property, live in one unit, and rent out the others. FHA loans allow 3.5% down on owner-occupied multi-family homes, which dramatically lowers the capital barrier. On a $700,000 duplex in Suffolk County, that means roughly $24,500 down instead of $140,000 or more. Rental income from the other unit offsets your mortgage, and in many cases covers it entirely.

Buy-and-hold rentals

Buy-and-hold is the most common strategy for building long-term wealth in Nassau and Suffolk Counties. You purchase a property, place tenants, and collect rent while the asset appreciates. Long Island rents are climbing 5–7% annually, with typical two-to-three-bedroom units renting between $2,400 and $3,200 per month. That rent growth, combined with historically strong appreciation in both counties, makes buy-and-hold a reliable path for patient investors.

BRRRR strategy

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. The concept is powerful: you force appreciation through renovation, then pull your equity back out via a cash-out refinance to fund the next purchase. The challenge on Long Island is that renovation costs are high, contractor availability is tight, and appraisals do not always reflect the full value of improvements. BRRRR works here, but it requires a conservative budget and a strong local contractor network.

Fix-and-flip

Fix-and-flip is the highest-risk strategy on Long Island. Carrying costs, property taxes, and contractor expenses eat into margins fast. A fix-and-flip project that runs three months over schedule can turn a projected $60,000 profit into a $10,000 loss. Experienced flippers succeed here by sourcing deeply discounted off-market properties and keeping renovation scopes tight.

| Strategy | Capital Required | Effort Level | Best For |

|---|---|---|---|

| House hacking | Low (3.5% FHA down) | Medium | First-time investors |

| Buy-and-hold | Medium (20–25% down) | Low ongoing | Long-term wealth builders |

| BRRRR | Medium to high | High | Experienced renovators |

| Fix-and-flip | High | Very high | Active investors with local networks |

Pro Tip: Pick one strategy and execute it twice before adding a second. Investors who scatter across multiple methods in year one rarely master any of them.

What market conditions must Long Island investors understand first?

Long Island’s real estate market rewards investors who study the numbers before they make an offer. The two most important variables are property taxes and rental demand, and both vary significantly between Nassau and Suffolk Counties.

Property taxes are the defining financial factor for any Long Island investment. Nassau County’s effective tax rate runs about 1.79%, while Suffolk County reaches up to 2.42%. On a $700,000 property in Suffolk, that translates to roughly $16,940 per year in property taxes alone. That figure appears in your cash flow calculation before you account for insurance, maintenance, or vacancy. Investors who ignore this number at the analysis stage consistently underperform.

The rental market, however, provides a strong counterbalance. Demand across Nassau and Suffolk remains high due to proximity to New York City, strong school districts, and limited new housing supply. Rents between $2,400 and $3,200 per month for standard units give investors a real income base to work with. The 5–7% annual rent growth rate means your income side of the equation improves each year, even as your fixed-rate mortgage payment stays flat.

Financing options shape how quickly you can grow. Conventional rental loans require 20–25% down, which on a $700,000 property means $140,000 to $175,000 in cash. FHA loans for owner-occupied multi-family properties cut that requirement to 3.5%, making house hacking the most capital-efficient entry point in this market.

Pro Tip: File a property tax assessment appeal within 30 days of your purchase closing. A successful protest can reduce your tax burden by hundreds of dollars per month, converting a marginal deal into a profitable one.

Street-level knowledge matters as much as county-level data. School district ratings, LIRR commute times, and neighborhood turnover rates all affect tenant quality and vacancy rates. A property in a top-rated school district in Smithtown or Garden City commands higher rents and attracts longer-tenured tenants than a comparable property in a lower-rated district nearby.

How do you start building your Long Island real estate portfolio step by step?

A clear sequence separates investors who close their first deal within 12 months from those who spend years preparing. Follow this order.

-

Assess your finances. Pull your credit report, calculate your liquid capital, and determine your debt-to-income ratio. Most lenders want a credit score above 680 for investment loans and above 620 for FHA owner-occupied financing. Know your number before you talk to anyone.

-

Get pre-approved. Work with a lender who has experience with Long Island investment properties. A pre-approval letter tells sellers you are serious and tells you exactly what price range you can target. Choose between FHA, conventional, and portfolio loan products based on your strategy.

-

Select your strategy. Match your strategy to your capital and schedule. If you have $30,000 in savings and a full-time job, house hacking is your starting point. If you have $200,000 and a flexible schedule, buy-and-hold or BRRRR become realistic options.

-

Source properties. Start with the MLS through a local agent who understands investor needs. Then build an off-market pipeline. Off-market deal sourcing through direct mail, probate attorneys, and investor networking groups is the primary way serious Long Island investors avoid bidding wars and overpaying.

-

Run your numbers. Calculate gross rent, subtract property taxes, insurance, maintenance (budget 10% of rent), vacancy (budget 5–8%), and mortgage payment. If the result is positive or close to break-even with strong appreciation potential, the deal deserves a deeper look.

-

Perform due diligence. Order a full home inspection, review the certificate of occupancy, and verify all permits on any prior renovation work. Unpermitted additions are common on Long Island and can create costly problems at resale or refinance.

-

Manage for growth. Use property management software like Buildium or AppFolio to track income, expenses, and maintenance requests from day one. Good records make your second and third acquisitions easier to finance.

Pro Tip: Attend local Real Estate Investors Association (REIA) meetings in Nassau and Suffolk Counties. The Long Island real estate tips you get from experienced local investors are worth more than any online course.

What mistakes do Long Island investors make most often?

The Long Island market punishes common mistakes more harshly than lower-cost markets because the numbers are bigger and the margins are thinner.

-

Underestimating property taxes. Investors who model cash flow using national average tax rates consistently get surprised. Always use the actual assessed value and current tax rate for the specific property, not county averages.

-

Overpaying in bidding wars. Competition in Nassau and Suffolk Counties is intense. Paying $50,000 over asking price to win a deal can eliminate two years of cash flow. Discipline at the offer stage protects your returns.

-

Ignoring carrying costs on flips. Renovation timelines on Long Island routinely run 20–30% longer than projected. Every extra month adds mortgage payments, taxes, and insurance. Budget for delays before you close.

-

Scaling too fast. Buying three properties in 12 months before you understand how to manage one is a common mistake among enthusiastic new investors. Each property is a business. Learn the operations before you multiply them.

-

Skipping the tax appeal. Protesting your tax assessment after purchase is one of the highest-return activities available to Long Island investors. Most skip it because they do not know it is an option.

“The investors I see succeed on Long Island are not the ones chasing the hottest strategy. They are the ones who pick one approach, learn it deeply, and execute it consistently over five or more years.”

Renovation budgets deserve a separate warning. Long Island contractors charge premium rates, and material costs have not retreated to pre-2020 levels. Add a 15–20% contingency to every renovation estimate. If you do not use it, you keep it. If you need it, you are covered.

Key takeaways

Building a real estate portfolio on Long Island requires strategy alignment, local market knowledge, and disciplined financial analysis from the first property forward.

| Point | Details |

|---|---|

| Start with house hacking | FHA financing at 3.5% down makes multi-family owner-occupancy the lowest-barrier entry point. |

| Model taxes precisely | Nassau and Suffolk tax rates reach 1.79–2.42%; use actual figures, not averages, in every deal analysis. |

| Source off-market deals | Bidding wars erode returns; build a direct mail and networking pipeline to find deals before they list. |

| Appeal your tax assessment | Filing a protest after closing can reduce annual taxes by hundreds of dollars and flip a marginal deal profitable. |

| Pick one strategy first | Mastering house hacking or buy-and-hold before adding BRRRR or flips prevents costly strategic drift. |

What I have learned from watching investors succeed and fail on Long Island

I have worked with buyers and investors across Nassau and Suffolk Counties long enough to see clear patterns. The investors who build real, lasting portfolios here are not the ones with the most capital at the start. They are the ones who respect the market’s specifics.

House hacking changed the trajectory for more first-time investors I have worked with than any other strategy. It is not glamorous. Living next to your tenants is not everyone’s preference. But it is the most honest way to learn property management, understand carrying costs, and build equity simultaneously. The investors who start there and stay disciplined almost always find their second deal within two years.

The mistake I see most often is investors treating Long Island like a national market. They read a book about real estate investing, apply generic cap rate targets, and wonder why nothing pencils out. This market has its own rules. School districts matter more here than in most places. The LIRR line a property sits near affects tenant demand in ways that no national data set captures. Local knowledge is not a soft advantage. It is the difference between a good deal and a bad one.

Long Island is not the easiest place to start investing in real estate. The prices are high, the taxes are real, and the competition is fierce. But the rental demand is durable, the appreciation history is strong, and the proximity to New York City creates a tenant base that does not disappear in a downturn. Play the long game here and the market rewards you.

— Andrew

Work with Andrewragusa to grow your Long Island investment portfolio

Andrewragusa brings deep knowledge of Nassau and Suffolk County markets to every investor relationship. Whether you are buying your first duplex through house hacking or expanding a multi-property portfolio, Andrew provides market analysis, off-market property sourcing, and direct guidance on where the numbers work in 2026.

Andrewragusa’s approach is built around helping investors avoid overpaying in competitive conditions and identifying properties with genuine cash flow potential. If you are ready to take your next step, connect with Andrew to get a personalized consultation on Long Island investment opportunities that match your goals and capital.

FAQ

What is the minimum capital needed to invest in Long Island real estate?

House hacking with an FHA loan requires as little as 3.5% down on an owner-occupied multi-family property. On a $700,000 duplex in Suffolk County, that is approximately $24,500 in down payment capital.

Which Long Island county is better for rental property investment?

Suffolk County offers lower median prices near $701,000 compared to Nassau’s $837,000, but carries a higher effective tax rate of up to 2.42%. Nassau offers stronger appreciation in many submarkets, making the right choice dependent on your cash flow versus appreciation priorities.

How do property taxes affect cash flow on Long Island?

Property taxes in Nassau and Suffolk Counties represent one of the largest fixed expenses in any rental property analysis. At 1.79–2.42% effective rates, annual tax bills on a $700,000 property range from roughly $12,530 to $16,940, which must be covered by rental income before any profit is realized.

What is the BRRRR strategy and does it work on Long Island?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It works on Long Island when investors source deeply discounted properties and control renovation costs tightly, but high contractor rates and unpredictable appraisals make it more challenging here than in lower-cost markets.

How do I find off-market properties on Long Island?

Building relationships with probate attorneys, estate sale companies, and local investor networks is the most reliable method. Off-market sourcing is critical on Long Island because listed properties frequently attract multiple offers that push prices above investment-grade levels.

Recent Comments